From Philosophy to Practice: 5 Daily Activities of a Focused Investor

“You need a well-defined investment philosophy to guide your decision-making process. Without one, you’re like a ship without a rudder." – Howard Marks

In our last blog we discussed the focus investment philosophy which we built from the ground up to fully leverage the MINDSET, SCOPE, and STRUCTURE advantages we have as retail investors.

It can be summarised as:

Find high quality businesses with meaning to you.

Buy with conviction when you are getting value.

Cultivate a business owners mindset and hold for the long term.

To implement the Focus Investment Philosophy, you need a process that you can follow on a day-to-day basis…

Day in the life as a Focus investor

When I first started investing, I had not properly honed my process. This led to a lot of time wasted and some poor decisions made. Ultimately these mistakes hurt my returns.

"It's good to learn from your mistakes. It's better to learn from other people's mistakes." - Warren Buffett

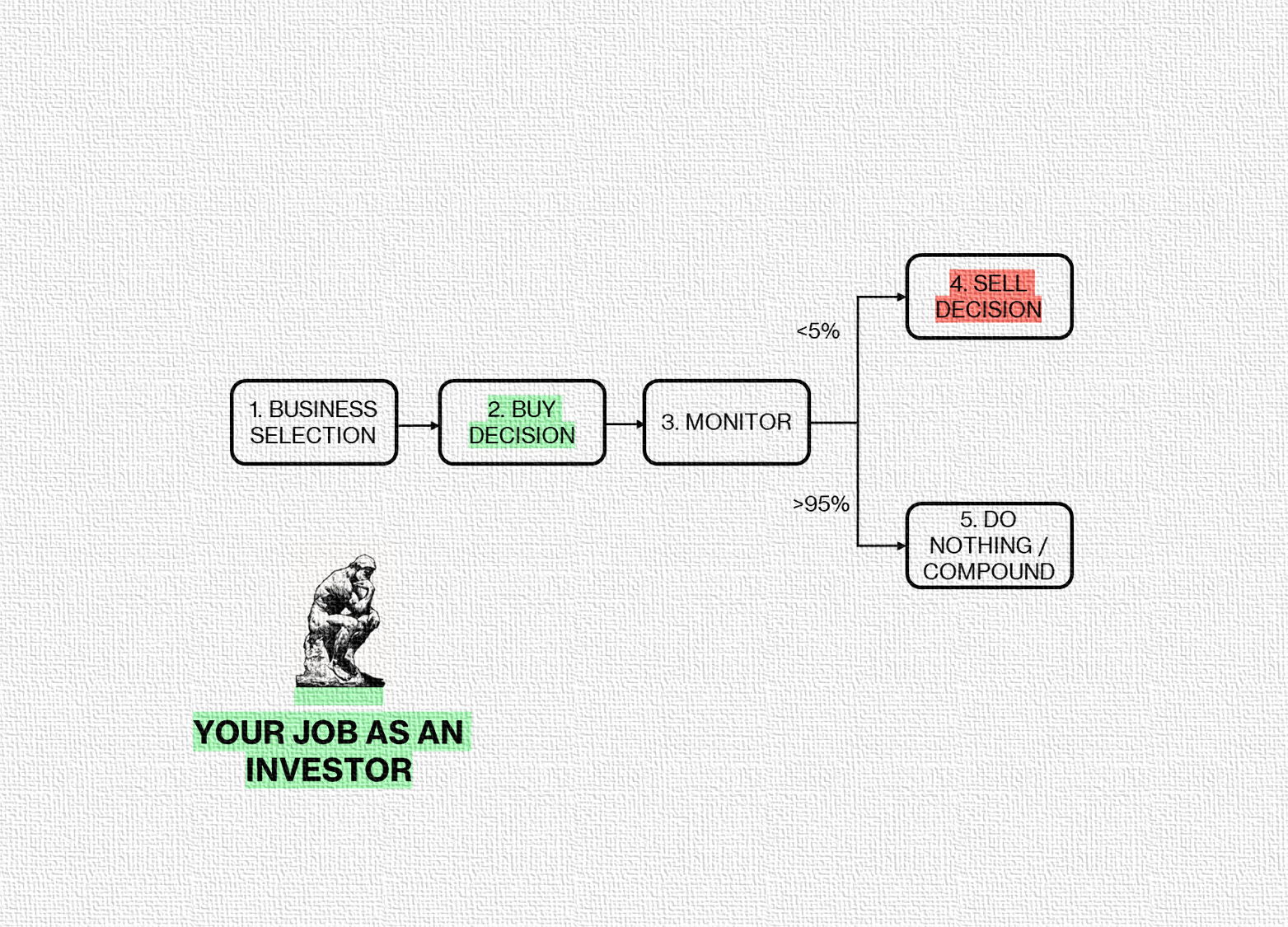

When you boil down what you need to do as an investor at the highest level there are only a few activities you need to perform based on decisions that need to be made.

In line with the investment philosophy this involves selecting high quality businesses, buying them when they represent excellent value, monitoring them for the long term and only selling when there is a legitimate reason.

"Investing is a process-driven endeavour. The key is to have a process and then follow it with discipline." – Mohnish Pabrai

By following this process, you will sidestep a large number of common investing traps and pitfalls.

We will cover only the high-level overview today and explore each area in more detail in future blog posts.

The process can be summarised as:

Step 1: Business Selection

Remember we are looking for high quality companies with meaning to you. We are also only interested in buying these companies when they present value to us.

There are over approximately 40,000 public stocks listed worldwide available for you to buy.

You need an efficient process to whittle this down to a concentrated list of possible buys.

To do this we will employ a selection funnel with a series of filters. These filters align with our investment philosophy and include:

Meaning: Invest in businesses you understand, find interesting and are comfortable supporting

Quality: Focus on companies with strong competitive advantages and consistent performance.

Management: Choose companies led by trustworthy, capable, and well-incentivized capital allocators.

Risk: Prioritize businesses with low debt and predictable earnings to minimize risk.

Value: Seek investments with a significant margin of safety between market price and intrinsic value.

The goal of these filters is to create a repeatable and efficient process that allows us to put companies into one of three buckets.

Too Hard: Companies that failed a filter and have been put in the too hard pile. This will represent the vast majority of stocks.

Watchlist: Quality companies at a price that does not represent good value.

Possible buy: Quality companies at a price that represents good value.

"We throw almost all decisions into a ‘too hard’ file and go onto the next one." – Charlie Munger

This is not to say that companies that make it into the too hard bucket are bad investments - some may well be great compounders. We are simply stating they are too difficult for us to have the conviction to invest meaningful amounts of capital into them. As Warren said:

"I don’t look to jump over 7-foot bars; I look around for 1-foot bars that I can step over." – Warren Buffett

The output of this process is to determine companies that are possible buys. The key word here is “possible”. Before actually making a purchase, you need to think about how this company fits into your wider portfolio as well as take the time assess your MINDSET.

This Buy Decision also needs a process…

Step 2: Buy Decision

Buying a single company should not be done in isolation. Just because you have found a high-quality company and a reasonable price it does not mean it is the best buy for you.

This is a key MINDSET principle – at any one time we are looking to deploy capital into the best ideas out of all possible ideas.

"The wise ones bet heavily when the world offers them that opportunity. They bet big when they have the odds. And the rest of the time, they don’t. It’s that simple.” – Charlie Munger

To do this you will need to review your current portfolio as well as the wider universe of stocks available to you. Consider the following questions:

Does this company represent the best use of my capital? Are there other options currently within my portfolio with better risk adjusted returns?

How does this company fit into my current portfolio? Are there any correlated risks that impact multiple holdings?

How much capital should I invest and what weighting should the investment be within the portfolio?

Any buy decision should be as measured and deliberate as possible.

For those who have read “thinking fast and slow” by Daniel Kahneman we are looking to employ system 2 thinking here to reduce the chance of jumping into a wrong decision. (p.s. those who have not should put it on their reading list!)

To support this time should be taken to:

Build a final concise thesis for the purchase. Taking the time to do this will slow the decision down and ensure you have considered all angles.

Confirm Key Performance Indicators (KPIs) that you will track moving forwards to assess progress against the thesis.

Take the opportunity to review your decision against a “Investing Mindset Checklist”. This checklist will include frequent questions designed to highlight any common misjudgements and biases we may have. (More to come on this in later blog posts)

“Checklists provide a cognitive net. They catch mental flaws inherent in all of us—flaws of memory and attention and thoroughness” - "The Checklist Manifesto" by Atul Gawande

Step 3: Monitor

Once purchased companies need to be monitored on an ongoing basis.

If you have done your job well in buying a small, concentrated set of quality companies for your portfolio then the burden here should be reduced.

The trick with monitoring your portfolio is taking a balanced approach:

On one hand we want to stay up to date with the company, its business fundamentals and anything effecting its intrinsic value.

On the other hand, we do not want to get lost in the minutiae of every press release and stock price change. Over monitoring can lead to rash decisions.

The key focus should be on the underlying business fundamentals and not the stock price or other people’s commentary.

Properly performing the steps within the “Buy Decision” will mean you have entered a position with your eyes open:

You have already built a thesis and know what key indicators to monitor.

You have bought the company for the long term and have a business owners mindset.

Your original purchase was based on the intrinsic value of the company, and you were not speculating on price.

This should help to reduce quick sell decisions.

However, there will be times when something happens that impacts your thesis and the fundamentals of the business.

At these points, a recalculation of the intrinsic value should be performed based on the latest updated business fundamentals. Where the intrinsic value of the business has deteriorated a sell decision needs to be made…

Step 4: Sell Decision

If you have picked quality companies, you should rarely be selling.

Remember we are looking to hold for the long term to let the magic of compounding take its course!

"Time is on your side when you own shares of superior companies." – Peter Lynch

As discussed in the buy decision - at any one time we are looking to deploy capital into the best ideas out of all possible ideas.

In that respect the sell decision is just the other side of the coin of the buy decision. If there are better opportunities, you should sell and deploy that capital elsewhere.

In practice there are only really a few valid reasons to sell:

Your intrinsic value for the stock is significantly below the current stock price because the business fundamentals have deteriorated.

Your intrinsic value for the stock is significantly below the current stock price because the stock price has increased without a corresponding increase in business fundamentals.

There are opportunities out there that represent a significantly better estimated rate of return.

You need the capital for a life event such as buying a house, putting your kids through school, retirement etc.

Given our business owners mindset and long-term perspective, a sell decision should not be taken lightly. There should be a significant burden of proof supporting one of the above reasons.

Again, like the buy decision this an opportunity to slow down and employ system 2 thinking:

Write a concise exit thesis

Demonstrate a deterioration against KPIs where applicable and the effect on intrinsic value

Take the opportunity to review your decision against a “Investing Mindset Checklist”.

After taking these steps you can be more confident in your decision to sell.

Remember most of the time you should be holding onto you winners, doing nothing, and letting the magic of compounding take hold…

Step 5: Compound

Great, so you have a portfolio of high-quality compounders, they are reasonably priced, and their business fundamentals are on track. What now?

Do nothing!

"The hardest thing to do is to do nothing." — John Bogle

For me this is the hardest part of investing. The reason I enjoy investing is I love studying businesses and how they work. This means I am always looking at potential investments.

If you are not careful this can lead to “Shiny Object Syndrome” which is the tendency to new and exciting ideas while neglecting existing ones.

Remember a solid strategy and sticking with what you know often leads to better results than constantly jumping to the next new thing.

To counteract this, you need to have more to your game than pure technical investing ability. You need to approach investing with the right mindset and practice:

Study your existing holdings: You should aim to be as knowledgeable as the management teams themselves. Remember, know what you own!

Compound your learning: Take the time to read and learn about other subjects. You will be surprised by how this can enhance your investing acumen.

Patience: Work on your mindset and develop the patience to hold your investments for the long term, focusing on business fundamentals rather than short-term market movements.

Conclusion

You should now have a sense of how the investment philosophy can be put into practice.

In the next couple of blog posts we will deep dive into Step 1: Business Selection.

Business selection is the meat and bones of the investment process and is the most technical in nature put of all the steps. Do not worry we will be simplifying the process down to what truly matters!

Disclaimer

As a reader of Focus Invested, you agree with our disclaimer. You can read the full disclaimer here.